")

Updated: April 2026 | Read Time: 5 mins | Team Opulnz Abode

The Hierarchy Has Shifted — And the Data Is Decisive

In Q1 2024, Delhi NCR accounted for 61% of all new luxury residential launches among India’s major cities — a commanding lead over Mumbai’s 26% and Bengaluru’s 19%. By 2025-26, the story has become even more definitive, but with important nuances that every serious buyer and investor needs to understand.

This is not just about which city sells more luxury units. It is about which city is reshaping what luxury means, at what price point, and for whom.

The 2026 Scoreboard — City by City

Delhi NCR — The Volume and Value Champion

Delhi NCR’s dominance in luxury residential is now structural, not cyclical. The numbers are staggering:

- NCR’s sales value jumped from ₹37,533 crore in 2021 to ₹1.83 lakh crore in 2025 — 400% growth in four years.

- Average ticket size: Rose from ₹0.89 crore to ₹3.64 crore — a 307% increase. No other Indian city comes close.

- Ultra-luxury dominance: 98% of units sold in Delhi and Gurugram are priced above ₹2 crore. Gurugram leads the ₹5 crore+ segment nationally at 64% share.

- NCR leads nationally: 25% value share of all India housing sales. Overtook Mumbai in value terms for the first time in 2025.

- Price growth: Delhi NCR recorded 19% year-on-year price growth in Q3 2025 — the highest of any major Indian city. Property prices in Gurugram have risen from ₹7,479/sq ft to ₹8,900/sq ft in one year.

- H1 2025 luxury leadership: Delhi NCR accounted for 57% (nearly 4,000 units) of all luxury unit sales across India’s top 7 cities — a threefold increase over H1 2024.

Mumbai — India’s Trophy Asset Capital

Mumbai may have ceded volume leadership to Delhi NCR, but it remains unchallenged as India’s trophy asset destination:

- Market share: 32.55% of India’s luxury residential market value in 2025, sustained by financial-sector wealth and limited coastline land supply.

- Three Sixty West benchmark: Prices at ₹1,00,000-1,50,000 per sq ft — India’s most expensive residential address. No other Indian city has a comparable per sq ft reference.

- Stamp duty collections: Rose over 20% year-on-year in early 2026, reflecting rising ticket sizes.

- Property registrations: Up 8% year-on-year in early 2026. Steady, not spectacular.

- Investment inflow: Mumbai MMR led institutional investment with 27% market share in 2025.

Mumbai’s story is not volume — it is value concentration and per sq ft ceiling-setting. Trophy asset psychology keeps demand intact even when volumes moderate.

Bengaluru — The End-User Powerhouse With High Rental Yields

Bengaluru’s luxury market is driven by end-users rather than speculation — IT professionals, startup founders, and MNC executives form its core buyer base:

- Price growth: 14% year-on-year in 2025 — second only to Delhi NCR.

- Rental yields: 4.45% gross — highest of any Indian city. Makes Bengaluru the most compelling rental income play in the luxury segment.

- Five-year CAGR: 10% — second only to Delhi NCR’s 11%.

- 2025 volumes: Declined 12% in overall sales but held firm in premium segments. Bengaluru, Mumbai, and Pune together accounted for 63% of housing sales.

- North Bengaluru surge: Q1 2026 saw 12,664 new launches in Bengaluru, with North (Devanahalli, Hebbal) accounting for 38% of city supply. Luxury homes made up 68% of launches in North Bengaluru.

The Rising Challengers — Chennai and Hyderabad

- Chennai: The dark horse of 2025. 31% sales growth — the strongest of any major city. 45% growth in new supply. Increasingly on the radar of developers expanding from South India.

- Hyderabad: Fastest-growing luxury city by CAGR — 12.60% projected through 2031, driven by technology sector inflows and airport corridor expansions in Kokapet and Narsingi.

Why Delhi NCR Broke Away from the Pack — The Structural Reasons

The NCR luxury surge is not luck. It is the product of specific, compounding structural advantages:

- Developer quality revolution: DLF, Godrej, Oberoi, Max Estates, Birla Estates, and Trump have collectively elevated product quality to global standards in Gurugram and Noida.

- Infrastructure acceleration: Dwarka Expressway, Golf Course Extension Road, Delhi-Meerut RRTS, Jewar International Airport — infrastructure investment has been relentless and impactful.

- Corporate wealth creation: Gurugram’s Cyber City and Noida’s technology corridor have generated enormous corporate wealth in a concentrated geography.

- NRI pipeline: NCR draws NRI capital from Punjabi, Haryanvi, and UP diaspora communities — one of India’s largest NRI capital pools.

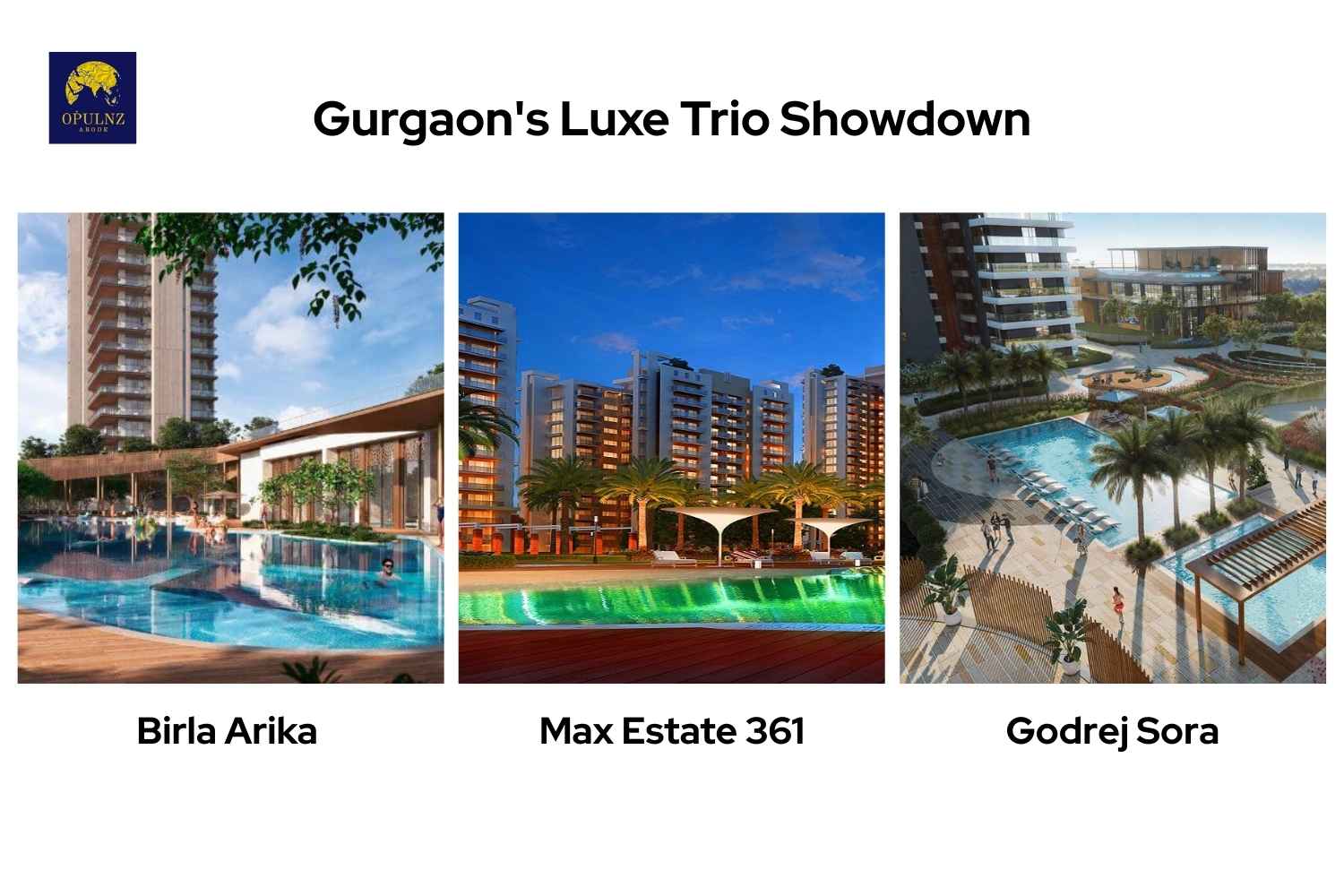

- Trophy aspirations: Delhi-NCR’s HNIs want homes that are global statements. The DLF Dahlias at ₹100 crore, Godrej Sora at ₹10 crore+, and Trump Towers at ₹18 crore+ are all finding buyers — a clear aspirational upgrade cycle underway.

For a detailed look at how NCR’s new wealth is being deployed across the luxury residential spectrum:

→ Godrej’s ₹5,000 Cr Launch Blitz: How India’s Largest Developer is Redefining Luxury Real Estate

The Investment Conclusion — Where to Buy in 2026

- Buy in Delhi NCR if: You want maximum capital appreciation (19% YoY price growth), the widest range of luxury product choices, and exposure to India’s fastest-growing luxury residential market.

- Buy in Mumbai if: You want trophy asset value, India’s highest per sq ft ceiling, strong NRI interest, and the most prestigious address in Indian real estate.

- Buy in Bengaluru if: You want the highest rental yields (4.45%), strong end-user demand, and exposure to India’s IT wealth creation engine. Best for income-oriented luxury investment.

- Watch Chennai and Hyderabad if: You want early-mover positioning in India’s next luxury frontiers — better value, higher growth potential, lower base.

For a global perspective on how India’s luxury residential market sits relative to the world’s finest addresses:

Further Reading from Superluxere

→ https://superluxere.com/blogs/prestige-gurugram-sector-92-first-project-2026

→ https://superluxere.com/blogs/nri-guide-buying-luxury-property-gurgaon-2026

→ https://superluxere.com/blogs/oberoi-elysian-goregaon-penthouse-mumbai

Which city leads India’s luxury real estate market in 2026?

Delhi NCR leads in volume, value growth, and new launches — with 57% share of all India luxury unit sales in H1 2025 and 400% sales value growth since 2021. Mumbai leads in per sq ft value and trophy-asset prestige. The two cities serve different buyer needs within India’s luxury market.

Has Delhi NCR overtaken Mumbai in real estate in 2026?

In value terms — yes. NCR has overtaken Mumbai in total housing sales value for the first time in 2025, holding a 25% national value share vs Mumbai’s 23%. In per sq ft luxury pricing and trophy-asset appeal, Mumbai remains the undisputed leader.

What is the luxury housing price growth in Delhi NCR in 2026?

Delhi NCR recorded 19% year-on-year price growth in Q3 2025 — the highest of any major Indian city. Gurugram specifically saw prices rise from ₹7,479/sq ft to ₹8,900/sq ft. The ultra-luxury Gurugram segment (₹10 crore+) recorded nearly 19% growth according to JLL data.

Why is Bengaluru’s luxury market different from Delhi NCR and Mumbai?

Bengaluru’s luxury market is end-user driven — IT professionals, startup founders, and corporate executives buying to live in, not purely to invest. This gives it the highest rental yields in India (4.45%) but lower speculative intensity than Delhi NCR. North Bengaluru is the emerging hotspot with luxury homes making up 68% of Q1 2026 launches.

Which Indian city has the highest luxury real estate appreciation potential in 2026-27?

Hyderabad is projected to have the highest luxury residential CAGR through 2031 at 12.60%, driven by technology sector growth and airport corridor development. Delhi NCR leads in short-term momentum. Chennai is the dark horse for upside-surprise appreciation.

Is India’s luxury real estate market sustainable in 2026?

The market is increasingly value-led rather than volume-led — which is a sign of maturity, not fragility. Properties above ₹1 crore accounted for 78% of all India residential sales in 2025. The structural drivers — HNI wealth creation, NRI investment, branded developer quality, infrastructure — are multi-year in nature, not cyclical.

Sources: CRE Matrix Pan India Real Estate 2025 | CBRE-ASSOCHAM H1 2025 | JLL Residential Dynamics Q4 2025 | Mordor Intelligence 2026 | Trade Brains 2026 | Superluxere Research 2026