")

Combination Blog | May 2026 | Read Time: 5 mins | Team Opulnz Abode

Sometimes a single month’s news tells you more about a market’s direction than a year of data analysis. In May 2026, three stories arrived within days of each other — each from a different angle, each adding a different dimension to the same underlying narrative. Together they are the clearest forward signal India’s luxury real estate market has produced.

Story 1 — The Developer Signal: DLF Guides ₹20,000 Crore ‘Comfortably’

When India’s largest listed developer uses the word ‘comfortably’ to describe a ₹20,000 crore target, the market should listen. DLF’s FY26 actuals (₹20,143 crore) met expectations. The FY27 guidance matches them — with room for growth. The Dahlias sold 32 units at ₹124 crore average in Q4 FY26 alone. HSBC and Citi both on Buy. The forward launch pipeline — Hamilton Court 2 GCR (₹8,000-9,000 Cr GDV), Oberoi Three Sixty North GCER already benchmarking ₹45,000 psf, Godrej Samaris GCR and Experion One42 GCR — is the most active in Indian luxury history.

The developer signal: India’s luxury market is not a peak — it is a base. The pipeline DLF is launching into is one they believe the market can absorb comfortably.

Story 2 — The Buyer Signal: $49.9 Billion in the UAE, Looking Home

Forbes 2026 confirmed nine UAE Indians at $49.9 billion combined wealth. This is the visible fraction of a far larger NRI UHNWI pool. At ₹84 to the dollar, $49.9 billion is ₹4.19 lakh crore — 17.4x Gurgaon’s entire 2025 ultra-luxury transaction volume. The buyer pool is not the constraint. The product quality has been — and in 2026, that constraint has been removed.

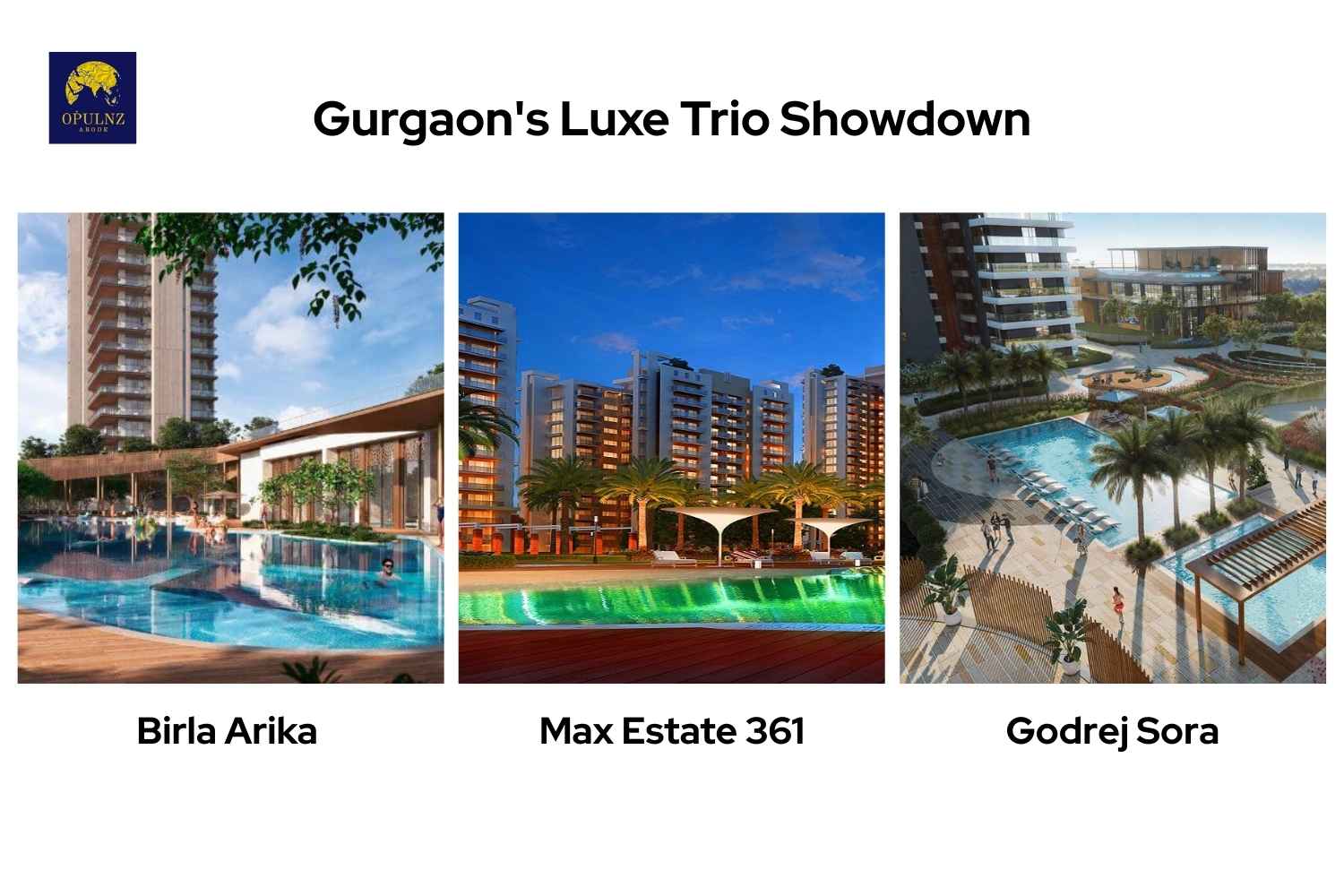

The convergence: DLF The Dahlias at 9,500 sq ft minimum compares to Singapore’s Sentosa Cove. Oberoi Three Sixty North’s private lift lobby compares to Dubai’s Address Residences. Max Estate 361’s intergenerational estate and Max Terraces’ Longevity Centre solve the NRI family’s senior parent problem professionally. On Noida Expressway, Max Estate 105 Sector 105 and Experion Windchants Nova Sector 112 add the value layer. And Experion 88A on Dwarka Expressway extends premium options across the corridor.

Story 3 — The Geographic Signal: Mumbai Is Not Conceding

Mahindra BeaconHill’s May 6 launch — 58 floors, 198 units, ₹1,650 crore GDV, RERA PM1170002600357 confirmed same day — is the geographic signal. Gurgaon may have won the volume crown. But Oberoi Three Sixty West Worli at ₹92,200 per sq ft resale is the permanent benchmark that tells every developer and every buyer what the ceiling of Indian residential luxury looks like. Mumbai’s response to Gurgaon’s surge is not to compete on volume — it is to widen the net of quality developers entering South Mumbai, as Mahindra’s BeaconHill demonstrates.

The Mumbai luxury wealth signals are unambiguous: the city’s UHNWI buyer base is expanding, the per sq ft ceiling is rising, and new supply from credible developers (Mahindra, Oberoi, and others in the pipeline) is being absorbed at launch. The geographic expansion of India’s luxury market — from Gurgaon-centric to simultaneously Gurgaon + Mumbai — is the third story’s message.

The Combined Reading — What the Three Stories Say About the Next Five Years

- By FY29: DLF alone may guide ₹30,000-35,000 crore in annual sales if FY27 closes above ₹20,000 crore. Other developers will track proportionately. India’s luxury residential market will cross USD 100 billion in total value before 2031.

- By 2028: Oberoi Three Sixty North possession. If it tracks Three Sixty West’s trajectory from even 50%, the ₹45,000 per sq ft pre-launch becomes ₹70,000-80,000 per sq ft. The GCER benchmark rises accordingly for every project that launches after it.

- By 2030: Jewar Airport is fully operational. Noida Expressway’s second appreciation wave has arrived. Max Estate 105 and Experion Windchants Nova buyers are sitting on 40-60% appreciation from entry. The buyer who waited for confirmation will pay 2031 prices.

- For the NRI reading this in May 2026: The three signals are aligned — developer confidence, buyer pool depth, geographic expansion. The window for current-cycle entry pricing is not permanently open.

Related Projects on Opulnz Abode

→ Opulnz Abode: DLF The Dahlias Sector 54 Golf Course Road

→ Opulnz Abode: Oberoi Realty Three Sixty North Sector 58 Gurgaon

→ Opulnz Abode: Max Estates Luxury Flats Noida Sector 128

→ Opulnz Abode: Experion Golf Course Road Sector 42 Gurgaon

→ Opulnz Abode: Luxury Flats in Gurugram — Full Portfolio

Frequently Asked Questions

What are the three May 2026 stories that define India’s luxury real estate direction?

First: DLF Q4 FY26 earnings (May 14) — ₹20,143 crore FY26, FY27 guidance ₹20,000 crore ‘comfortably,’ 60% Dahlias sold, HSBC and Citi on Buy. Second: Forbes 2026 UAE Indian billionaires — 9 Indians at $49.9B, confirming NRI UHNWI buyer pool depth. Third: Mahindra BeaconHill Mahalaxmi launch (May 6) — ₹1,650 crore GDV, RERA confirmed same day, marking Mumbai’s luxury developer base widening.

What is the five-year outlook for India’s luxury real estate market?

Mordor Intelligence projects USD 107.99 billion by 2031 (from USD 64.21 billion in 2026) at 10.95% CAGR. UHNWI base grows 12-15% annually. Infrastructure convergence — Jewar Airport, Delhi Metro Phase 4, RRTS — triggers appreciation cycles. NRI capital allocation accelerating as product quality closes gap with global benchmarks. Five-year direction: unambiguously upward across Gurgaon, Mumbai, and the emerging Noida corridor.

Which Superluxere project pages are most relevant for a 2026 luxury buyer?

GCR buyers: DLF Dahlias and Godrej Samaris project pages. GCER buyers: Oberoi Three Sixty North and Experion One42 project pages. DXP buyers: Max Estate 361 and Max Terraces project pages. Noida buyers: Max Estate 105 project page. Mumbai reference: Oberoi Three Sixty West Worli project page. All at superluxere.com — the most comprehensive analytical resource for NCR and Mumbai ultra-luxury.

Is Mahindra Lifespaces reliable for a long-term luxury project?

Yes. Cash-surplus balance sheet (negative net debt-to-equity March 31, 2026). FY26 pre-sales ₹3,405 crore (+55% YoY). GDV pipeline ₹45,180 crore. Mahindra Group — 130+ year enterprise. RERA PM1170002600357 confirmed May 6, 2026. ICICI Direct and HDFC Securities both on Buy.

Does the Jewar Airport affect Gurgaon luxury property values?

Yes — indirectly and directly. Directly: Sector 102 Gurgaon (Adani The Marq, BPTP Sector 113) — IGI Airport 15-20 minutes. Jewar at 40-45 km becomes the second airport for Gurgaon’s frequent flyers. Indirectly: Noida Expressway’s luxury corridor (Max Estate 105, Experion Windchants Nova) benefits primarily — but the airport’s economic halo (employment, logistics, aviation-adjacent businesses) extends appreciation across the entire NCR luxury belt.

How do these three signals change the buy-now-or-wait calculation?

They align uniformly toward acting. DLF’s ₹20,000 crore confidence means new launches will price above current benchmarks — Hamilton Court 2 GCR will price above Godrej Samaris. Oberoi Three Sixty North at formal launch will price above current EOI. Mahindra BeaconHill at any project update will price above current Day 1 pricing. Waiting costs money in a market where every credible new launch prices above the previous one.

Sources: Fortune India | Financial Express | Construction World | Business Standard | Forbes World’s Billionaires 2026 | DLF Q4 FY26 Earnings | Mahindra Lifespaces May 6 2026 | Mordor Intelligence | India Sotheby’s Luxury Report 2025 | Superluxere Research 2026

Superluxere analysis: superluxere.com/blogs